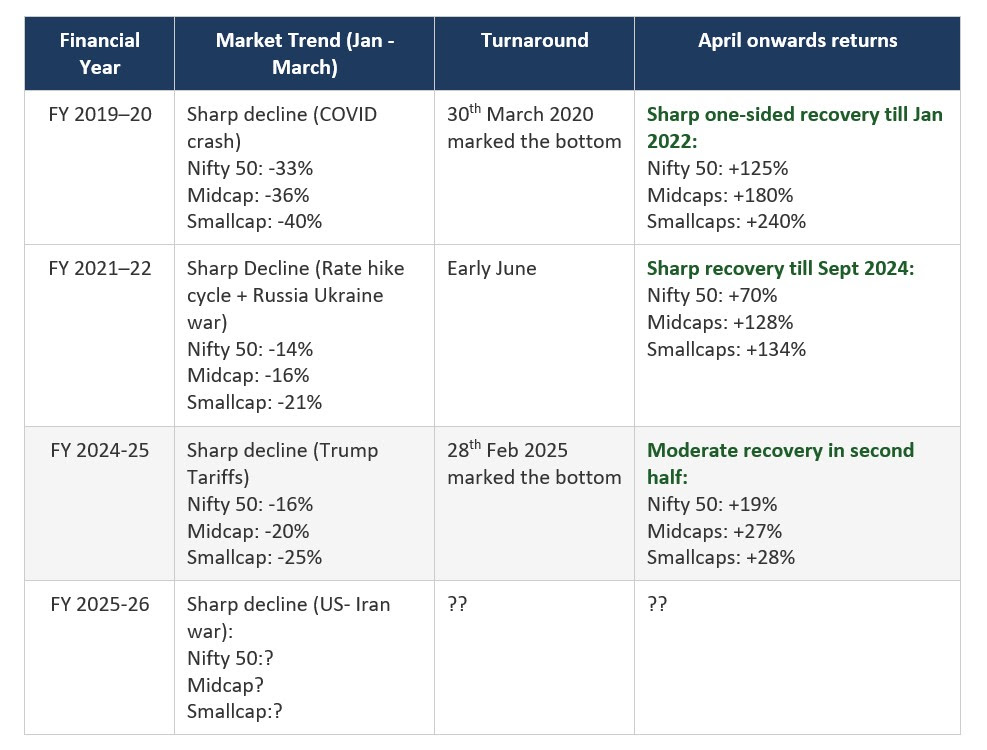

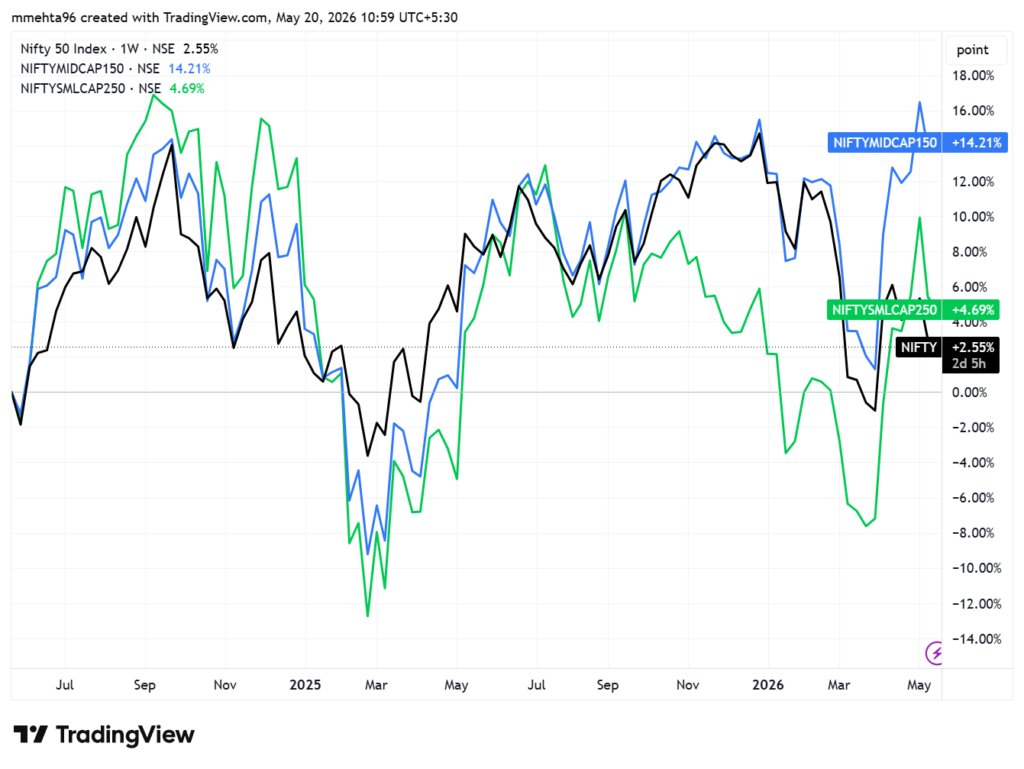

Investors who entered the markets in the last 2 years have increasingly been asking the question — “Where are my returns?”

This concern is understandable, as the Nifty has largely been hovering in the 24,000–26,000 range for nearly two years despite multiple phases of volatility and global uncertainty.

While such periods may feel unusual for first-time investors, market consolidation after strong rallies is a natural part of investing. Investors who have been through multiple market cycles over the last 5–10 years know that these phases often create the best opportunities to accumulate quality assets at reasonable valuations.

The global environment continues to remain uncertain with ongoing geopolitical tensions, trade disruptions, elevated interest rates, and slowing growth across major economies. However, despite these challenges, India continues to stand out relatively better due to strong domestic consumption, government spending, improving manufacturing ecosystem, stable banking system, and rising participation in financial markets.

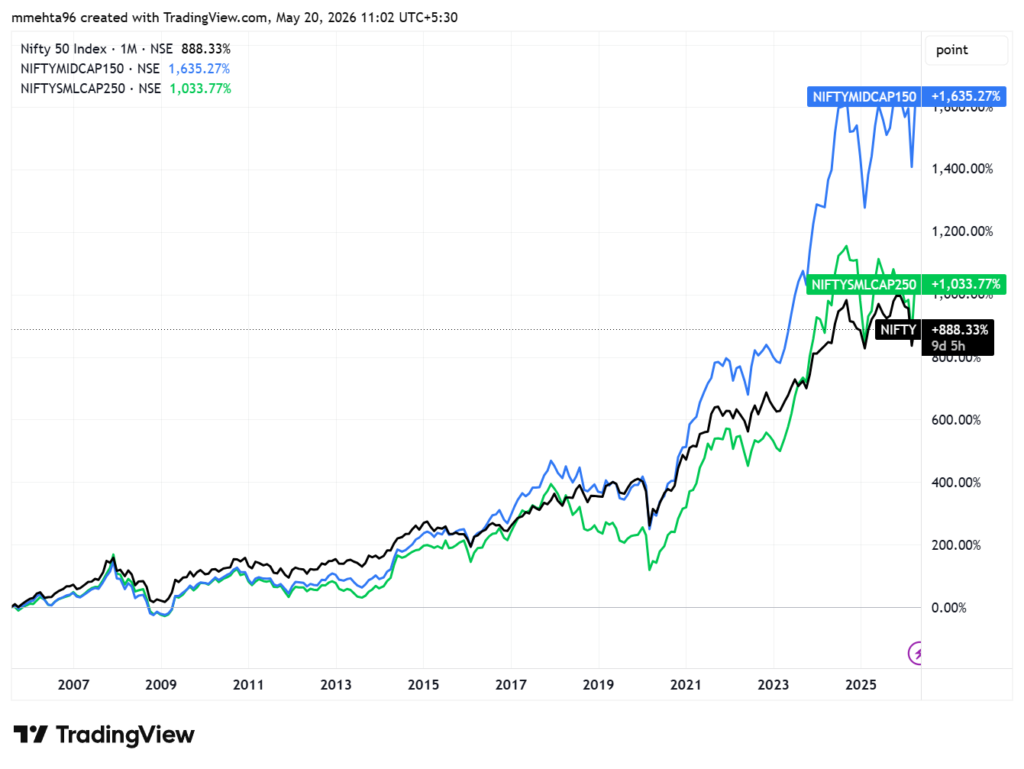

Historically, wealth creation in equities has not happened in a straight line. Markets often spend time consolidating before the next phase of growth begins. The first few years of investing may sometimes appear “boring,” but the real power of compounding becomes visible only over longer holding periods.

What Should Investors Do?

Continue SIPs with discipline and consistency.

Avoid panic during corrections and volatility.

If possible, consider averaging investments during meaningful market declines (10%–20% corrections).

Stay invested according to your long-term asset allocation strategy.

Avoid speculation, leverage, and short-term market predictions.

Focus on goals, not temporary market movements.

Equity investing is a long-term journey. Temporary periods of low returns are part of the process, but disciplined investors who stay invested through cycles are often the ones who benefit the most over time.

THE WILL — Your Final Word

THE WILL — Your Final Word Anyone who owns property — residential, commercial, or agricultural

Anyone who owns property — residential, commercial, or agricultural THE TRUST — Wealth on Your Terms

THE TRUST — Wealth on Your Terms THE HUF — A Smart Tax Structure for Families

THE HUF — A Smart Tax Structure for Families SO, WHERE DO YOU BEGIN?

SO, WHERE DO YOU BEGIN?