What No One Tells You — Until It’s Too Late

The Retirement Conversation India Keeps Avoiding

Retirement is not an event. It is a state of financial independence that you either plan for — or stumble into unprepared. In India, we are good at planning weddings, children’s education, and home purchases.

But retirement? That conversation gets pushed to ‘later’. The problem with ‘later’ is that it is the most expensive word in personal finance.

This note is our attempt to change that conversation. We want to put hard numbers in front of you — not to alarm, but to empower. Because the best time to plan your retirement was the day you earned your first rupee. The second best time is today.

Reasons Why Retirement Planning is Non-Negotiable?

1. No Government Safety Net — You Are On Your Own

Unlike citizens of the UK, US, or Germany, the vast majority of Indians have no universal state pension or social security to fall back on. The EPFO covers organised-sector employees and the NPS exists — but the amounts they generate are rarely sufficient to maintain one’s pre-retirement lifestyle. The government cannot be your retirement plan. You must be your own retirement plan.

The Harsh Truth

Less than 12% of India’s workforce has access to any formal pension. The remaining 88% must self-fund their entire retirement. That includes most business owners, professionals, and self-employed individuals.

2. Skyrocketing Healthcare Expenses

Medical inflation in India runs at 12–14% per annum — nearly double the general rate of inflation. As we age, healthcare consumption rises dramatically. A hospitalisation that costs ₹3 lakhs today will cost ₹30 lakhs in 20 years. Add to this chronic conditions, specialist consultations, home nursing, and long-term care — and healthcare alone can consume 25–35% of a retiree’s annual budget.

Key Data Point

A couple retiring today at 60 may need ₹1–1.5 Crore earmarked purely for healthcare over their retirement years — even with health insurance. Post-retirement, insurers often restrict coverage or charge prohibitive premiums.

3. Rising Life Expectancy — The Good Problem

India’s average life expectancy has risen from 59 years in 1990 to 70+ years today, and urban, educated, health-conscious individuals regularly live to 85–90. This is a triumph of medicine and nutrition. But financially, it is a challenge: you may need to fund 25–35 years of post-retirement life. Running out of money at age 80 is not a theoretical risk — it is a very real one for those who underestimate longevity.

Plan For 90, Not 75

We always build retirement plans assuming a life expectancy of at least 85–90 years. It is far better to have surplus than to outlive your money.

4. Inflation — The Silent Wealth Eroder

At a sustained 6% inflation, the value of money halves every 12 years. ₹1 lakh today will buy what ₹17,000 buys in 30 years. This means your retirement corpus cannot just be ‘large’ — it must be invested and growing even after retirement. A fixed deposit strategy post-retirement is a slow path to poverty. Your post-retirement portfolio must beat inflation consistently.

5. The Death of Joint-Family Financial Support

For generations, Indian retirement relied on an implicit social contract: children would support ageing parents. That contract is rapidly breaking down. Nuclear families, children moving to different cities or countries, rising costs of living, and shifting social norms mean you cannot and should not build your retirement plan around financial support from your children. Expecting your children to fund your retirement is also an unfair burden on their financial journey.

6. Lifestyle Inflation — You Won’t Want to ‘Cut Back’

Most people assume they will ‘live simply’ in retirement. The reality is often the opposite. With more time and fewer obligations, retirees tend to travel more, eat out more, pursue hobbies, and spend on grandchildren. A comfortable retirement is not a frugal one. Plan for the lifestyle you want — not a diminished version of it. Your retirement corpus must fund your aspirations, not just your survival.

7. No Income, But Fixed Costs Remain

When you retire, your salary stops. But your EMIs, utility bills, maintenance costs, insurance premiums, and day-to-day expenses continue unabated. The shock of going from a monthly income to zero income — while expenses persist — is one of the most underestimated financial transitions. Without a well-structured retirement corpus and withdrawal plan, this transition can be deeply destabilising.

8. Tax-Inefficient Withdrawal Without Planning

Unplanned retirement assets — lumped in FDs, real estate— often generate income that is fully taxable, leaving retirees in higher tax brackets than expected. Proper retirement planning involves not just accumulation, but structured, tax-efficient withdrawal. The right asset mix — equity mutual funds, debt funds, NPS, REITs — can dramatically reduce your post-retirement tax burden and extend corpus longevity.

Finding Your True Retirement Corpus — A Step-by-Step Framework

Most people guess a round number — ₹5 crore or ₹10 crore — and work backwards. That is the wrong approach. Here is the right one:

Step 1: Define Your Retirement Lifestyle

Start with today’s monthly expenses — not what you think you’ll spend in retirement, but what you spend right now. Be honest and comprehensive: rent or maintenance, groceries, utilities, dining, travel, medical, insurance, leisure, and charitable giving. This is your baseline.

• List all current monthly expenses in writing

• Add categories you currently don’t spend on but will (medical aids, leisure, travel)

• Deduct expenses that will stop (children’s education, EMIs that will end)

• Arrive at a realistic monthly retirement lifestyle number

Onesta Recommendation

Most of our HNI clients find their retirement monthly expense target is 70–90% of their current spending — not 50% as commonly assumed. Comfort does not shrink in retirement; it often expands.

Step 2: Adjust for Inflation — Find the Future Value of Monthly Expenses

The amount you need per month at retirement is NOT what you need today. You must project it forward at 6% annual inflation. Use this formula: Future Monthly Need = Current Monthly Expense × (1.06)^Years to Retirement

Example: If you need ₹1 lakh per month today and you retire in 25 years, you will need ₹4.3 lakhs per month at retirement just to maintain the same lifestyle. This step shocks most clients — but it is reality.

Step 3: Determine Your Retirement Duration

Calculate how many years your corpus must last. We recommend planning to age 90 as a minimum, and to age 95 for those with strong family longevity histories.

• Retiring at 50 → Plan for 40–45 years of post-retirement life

• Retiring at 60 → Plan for 30–35 years of post-retirement life

• Always err on the side of living longer — surplus is a gift, shortage is a catastrophe

Step 4: Calculate the Corpus — The Inflation-Adjusted Annuity Method

Your corpus must generate an income that keeps pace with inflation throughout your retirement. Using a 7% post-retirement portfolio return and 6% inflation, the ‘real’ return is approximately 1%. This gives us a corpus multiplier:

• Retiring at 50 (35-year retirement): Corpus ≈ 28× your annual expense at retirement

• Retiring at 60 (25-year retirement): Corpus ≈ 21× your annual expense at retirement

Formula: Corpus = (Monthly Expense at Retirement × 12) × Multiplier

Step 5: Account for Healthcare and Emergency Buffers

Add a dedicated healthcare and contingency reserve over and above the lifestyle corpus. We recommend ₹50 lakhs–₹1.5 crore for a couple depending on current health status, family medical history, and existing health coverage.

• Senior citizen health insurance (review coverage annually)

• Critical illness and personal accident covers

• ₹25–50 lakh liquid emergency fund separate from the retirement corpus

Step 6: Identify and Audit Existing Assets

Now inventory what you already have working towards retirement: existing mutual fund investments, PF and EPF balance, NPS Tier 1 corpus, LIC endowment maturity values, real estate rental income, and any other assets. Calculate their future value at your target retirement date assuming 10–12% growth for equity and 6–7% for debt assets.

Important Note

Do not count your primary residence as a retirement asset unless you genuinely plan to sell or reverse-mortgage it. Most people don’t — and shouldn’t be forced to.

Step 7: Identify the GAP — Then Bridge It

Gap = True Retirement Corpus Required minus Future Value of Existing Assets. This gap is what your systematic investments must fill. Now you know exactly what you need to save and invest every month — or as a lump sum today — to reach your retirement goal.

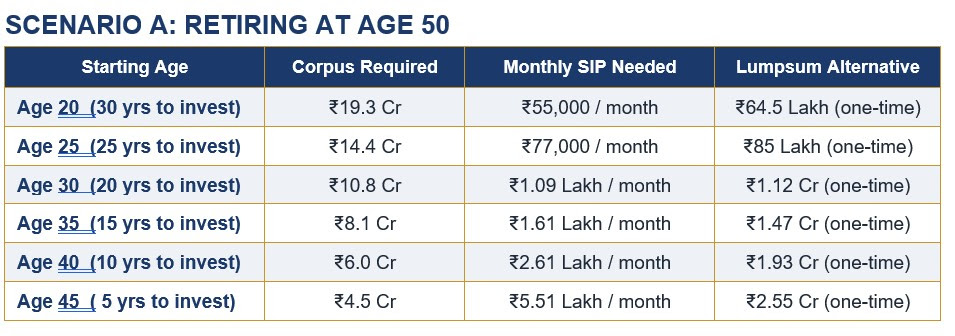

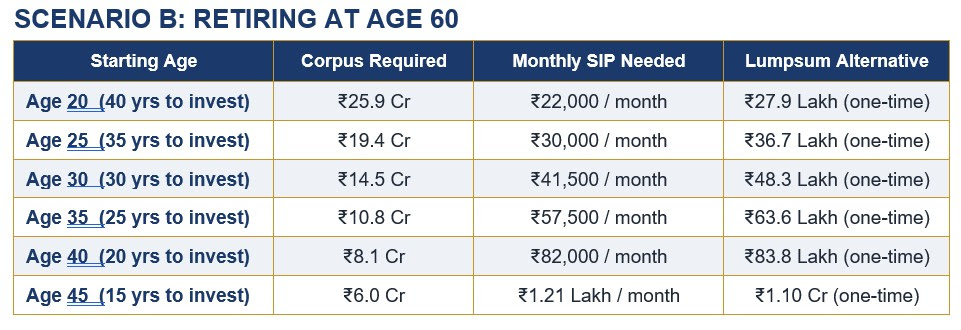

The Numbers: What You Need at Every Starting Age

Assumptions: Current monthly lifestyle expense: ₹1 Lakh (today’s value) | Inflation: 6% p.a. | Pre-retirement investment return: 12% p.a. | Post-retirement portfolio return: 7% p.a. | Retirement duration planned to age 85. Healthcare and emergency corpus are additional.

* SIP assumed at 12% p.a. return via diversified equity mutual funds. Lumpsum amount to be invested today at 12% p.a. SIP amounts are for ₹1L/month current lifestyle — scale proportionally for your actual expenses

* Same assumptions as Scenario A. Retiring at 60 benefits significantly from the extra decade of compounding — note how the required SIP is dramatically lower compared to retiring at 50.

The Most Important Insight from These Tables

The difference between starting at age 20 versus age 35 for a retirement at 60 is not a 15-year gap — it is the difference between a ₹22,000 SIP and a ₹57,500 SIP for the same retirement corpus. Compounding rewards patience exponentially. Every year you delay costs you not just one year — it costs you the compounding of that year times 30–40 future years.

How to Scale These Numbers for Your Lifestyle: If your current monthly expense is ₹2 lakhs, multiply all figures by 2. If it is ₹1.5 lakhs, multiply by 1.5. The proportionality is direct.

Hard Facts About Retirement — No Sugarcoating

HARD FACT #1: THERE IS NO LOAN FOR RETIREMENT

Think about every major financial goal in life: You can take a home loan for a house. You can take an education loan for your children. You can take a car loan, a business loan, a gold loan. But there is absolutely no bank, no NBFC, no institution on earth that will give you a ‘retirement loan’. No one will lend you money to fund 30 years of post-retirement life.

This single fact should change everything about how you approach retirement savings. Because every other financial goal has a recovery option — retirement does not. If you miss buying a house, you can rent. If you can’t fund education, there are scholarships and loans. But if you run out of money at age 75, there is no safety net. No bailout. No second chance.

The Blunt Truth

Your children may help. Your savings may stretch. But dignity, independence, and the ability to meet your own healthcare needs — these require a corpus that only YOU can build, starting NOW. The alternative is financial dependence in old age, and that is a deeply uncomfortable position for anyone who has worked hard all their life.

Hard Fact #2: Delaying by 5 Years Doubles Your Required SIP

Look at the tables above. The jump from starting at 30 to starting at 35 (for retirement at 60) takes the required monthly SIP from ₹41,500 to ₹57,500 — a 38% increase for the same outcome. From 35 to 40, it jumps to ₹82,000 — a doubling. Time, once lost, cannot be bought back at any price. A gym membership unused for a year means you restart fitness. An investment SIP missed for five years means you restart compounding — and compounding has no ‘restart’ button.

Hard Fact #3: Your Real Estate Is NOT Your Retirement Plan

Many Indian families hold a significant portion of their wealth in real estate, believing it is their ‘retirement asset’. Real estate is illiquid, expensive to maintain, subject to rental vacancies, and practically impossible to partially redeem. You cannot sell one bedroom of your flat when you need ₹5 lakhs for a medical emergency. Unless you have a structured rental income stream and a clear plan to eventually liquidate, real estate should not be counted as your primary retirement asset.

Hard Fact #4: Fixed Deposits Will Not Save You

A retiree with ₹2 crore in FDs at 7% earns ₹14 lakhs a year or ₹1.17 lakhs a month. After tax (at 30% bracket), this becomes ₹81,900 per month. With 6% inflation, this purchasing power falls to ₹45,800 in 10 years and ₹25,600 in 20 years — in today’s rupees. The FD corpus itself stays nominally the same but loses real value every year. FDs are not a retirement strategy. They are a retirement risk.

Hard Fact #5: Equity Is Not Optional for Retirement

Given inflation at 6% and the need for a retirement portfolio to last 25–35 years, equity exposure is not speculative — it is essential. Even at age 60, a well-managed portfolio should have 30–50% in equity to ensure the corpus does not deplete prematurely. The fear of market volatility must be weighed against the certainty of inflation erosion. We help clients navigate this balance with structured, age-appropriate asset allocation.

What You Should Do Next

Retirement planning is not complicated. But it requires honesty, discipline, and the willingness to start. Here is your action list:

• Write down your current monthly expenses — every rupee

• Decide your target retirement age

• Use the tables in this note as a first-level estimate of your SIP requirement

• Schedule a retirement planning session with your Onesta advisor

• Review and revise your plan every 2 years or after any major life event

• Do NOT pause SIPs during market downturns — they are your retirement’s best friend

“The best time to plant a tree was 20 years ago. The second best time is now.”

— Chinese Proverb | The wisdom of every retirement advisor, ever.