India transformed in less than a decade; different from 2013: Morgan Stanley

This India is different from what it was in 2013. In a short span of 10 years, India has gained positions in the world order with significant positive consequences for the macro and market outlook, Morgan Stanley said in a report.

Ten big changes, mostly because of India’s policy choices, and their implications for its economy and market were highlighted in the report:

Supply-side Policy Reforms: Infrastructure has picked up & corporate tax at par with peer countries;

Formalisation of the economy: GST collection on an upward trend & digital transactions as % of GDP at record high;

Real Estate (Regulation and Development) Act;

Digitalizing Social Transfers;

Insolvency and Bankruptcy Code;

Flexible Inflation Targeting;

Focus on FDI;

India’s 401(k) Moment: SIP, NPS and EPF investment in equities at record high;

Government Support for Corporate Profits;

MNC Sentiment at Multiyear High: India’s service export market share accelerates.

The ten macroeconomic and stock market implications of the aforesaid changes:

Manufacturing and capex as % of GDP to increase steadily: the share of both to rise in GDP by approximately 5ppt by 2032;

Export market share to double: Export market share will rise to 4.5% by 2031, nearly 2x from 2021 levels;

Major shift in consumption basket: As India’s per capita income increases from US$2,200 currently to about US$5,200 by F2032, this will have major implications for change in the consumption basket, with an impetus to discretionary consumption;

Lower volatility in inflation and shallower interest rate cycles: Shallower rate cycles could also imply more benign equity market cycles;

Benign trend in current account deficit

A profit boom: The share of profits in GDP has doubled from all-time lows hit in 2020 and are set to rise further – maybe even double from here – leading to strong absolute and relative earnings. This explains India’s apparently rich headline equity valuations.

Lower correlation with oil prices: Lower share of foreign portfolio (FPI) in current account funding has reduced the stock market’s negative return correlation with oil prices, especially when oil prices rise due to supply disruption.

Lower correlation with US recession: As India’s reliance on global capital market flows has reduced, the market’s sensitivity to a US recession and US Fed rate changes also seems to be fading.

Valuation re-rating: This reflects persistent domestic demand for stocks and higher growth for longer. India is trading at a premium to long-term history, albeit well off highs and in line with recent history.

India’s beta to EM has fallen to 0.6: This is a consequence of improved macro stability and reduction in dependence on global capital market flows to fund the CAD.

Credits: Brian Feroldi

Quote of the month

You cannot sow something today and reap tomorrow! A seed has to go through the various seasons before it turns into a fully grown tree. So is the case with investing

-Parag Parikh

From the global leaders:

“We are at the start of a new long-term bull run for Indian markets”: Mark Mobius, Mobius Capital

“Political stability helping drive investments to India”: Chip Bergh, CEO, Levi Strauss

“India Is in Such Wonderful Hands”: US Ambassador Eric Garcetti

“India and Mexico ‘Best Structural Stories in Emerging Markets”: Global X

Indian macro dataflow remained strong:

Manufacturing PMI: Manufacturing PMI at 31-month high of 58.7 in May on robust demand for new orders and remained in expansion zone (>50 points) for the 23rd straight month;

Services PMI: The Indian services PMI declined to 61.2 in May after reaching a 13 year high of 62 in April 2023. It remained in expansion zone (>50 points) for the 22nd straight month;

GST Collection: Gross GST collection for May 2023 stood at Rs. 1.57 lakh crore as against Rs. 1.41 lakh crore for May 2022, registering a growth of 12%;

Credit growth: Credit growth reached 15.42% YoY as of 19th May 2023 against YoY growth of 11.14% as observed on 20th May 2022;

Inflation: India’s retail inflation eases to more than 2-year low of 4.25% in May;

Forex: India’s foreign exchange reserves stood at $595.1 billion as of June 2.

Equity:

SENSEX grew by 2.5% in May.

BSE Mid-cap and small-cap indices outperformed large-cap indices and were up 6.3% and 5.6%, respectively

Sector-wise, all but two sectors ended in green, namely metals (-2.9%) and oil & gas (-1.6%). Auto (+7.9%), Realty (+7.7%) and IT (+6.7%) indices were the largest gainers.

Among the top gainers globally were Japan (+7.0%), Taiwan (+6.4%) and Brazil (+3.9%). Meanwhile, Hong Kong (-8.3%), the UK (-5.4%) and France (-5.2%) were the most affected;

FIIs (Foreign Institutional Investors) continued to be net buyers of Indian equities in May (+Rs. 38,093 crore);

Mutual fund SIP flows hit new high of Rs. 14,749 crore in May.

Fixed income:

The US Federal Reserve in its May-23 policy meet, raised the Fed Funds Rate by 25 basis points to 5%-5.25%;

The European Central Bank raised its key interest rates by 25 basis points during its May meeting;

The Bank of England raised the bank rate by 25 basis points to 4.5% at its May policy meet;

10 year G-Sec rallied to sub 7% as as the US yields dropped sharply post FOMC meet wherein Fed signalled a likely end to the rate hiking cycle. 10-year

benchmark traded in a range of 6.95%-7.13% during the month;

System liquidity remained in surplus with average monthly liquidity coming down to Rs. 72,594 crores surplus vs a surplus of Rs. 1,53,205 crores in the month of April.

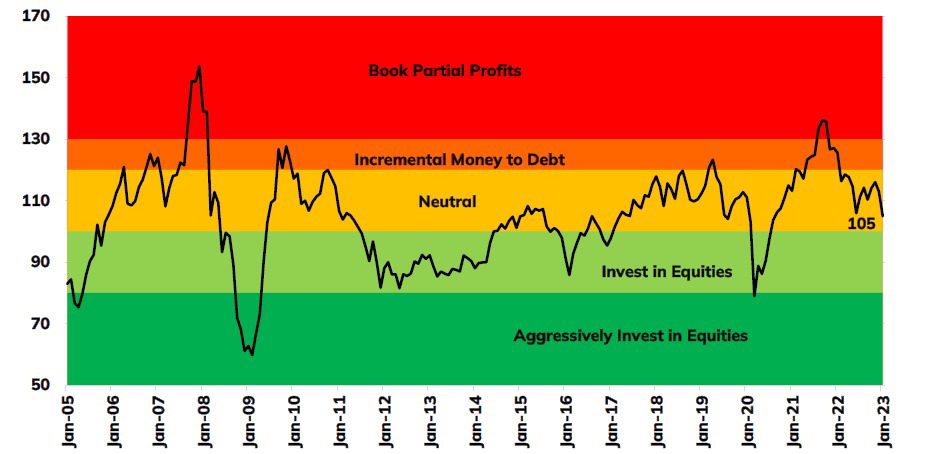

Outlook:

Post March-2023, equity valuations have moved higher due to renewed interest from FIIs. India’s strong macro-economic situation has led to positive overall sentiments.

We are in a neutral situation where equities cannot be avoided due to strong macros, nor it is recommended to be overweight on equities, due to valuations.

The Union Budget’s focus on higher Capital Expenditure by the Centre & States; push for consumption through lower taxes and goal of fiscal consolidation, together underpin India’s growth.

Companies have started deploying the excess profit, as evidenced by the increase in ordering activity – a precursor to increase in private Capex. We should see an investment driven economic growth starting FY24E.

We expect that strong demand scenario (domestic and international businesses), softening raw material inflation, easing global supply chains, eventual pick up in rural income as rural economy responds to increasing government infrastructure spends and benefits from improved crop prices and sharp surge in consumption spending due to wedding season should help achieve broad based domestic growth in coming quarters. Hence, we are overweight on domestic demand related sectors as growth and earnings certainties may be higher in related segments

Disclaimer: The views expressed herein constitute only the opinions/ facts and do not constitute any guidelines or recommendations on any course of action to be followed by the reader. This information is meant for general reading purposes only and is not meant to serve as a professional guide for the readers