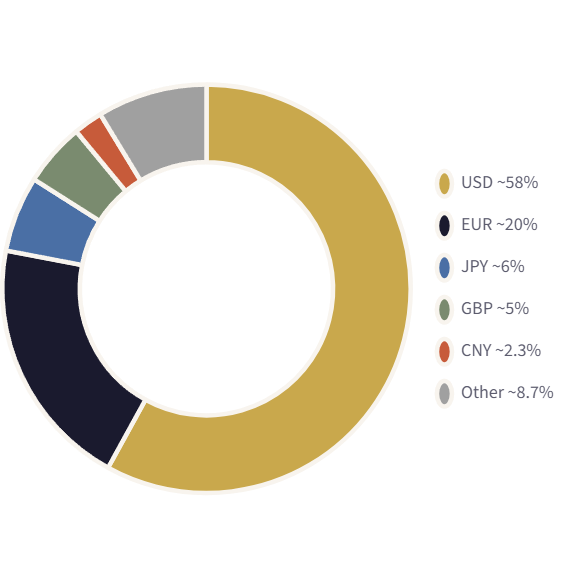

~58% Global FX Reserve Share (USD)

~90% FX Trades Involve USD

~80% Global Oil Trade in USD

In an era of rising multipolarity, deglobalization pressures, and growing calls for de-dollarization, one question dominates macro discussions: can anything dethrone the U.S. dollar? In this edition, we lay out the structural, financial, and geopolitical architecture that keeps the greenback at the apex of the global monetary system — and what risks, if any, could alter this hierarchy.

01 — Reserve Currency Status

The Dollar’s Iron Grip on Global Reserves: The USD has served as the world’s primary reserve currency since the Bretton Woods Agreement of 1944. Central banks globally hold dollars to settle international trade, service dollar-denominated debt, and manage currency volatility. Despite decades of speculation about its decline, the dollar’s reserve share has remained broadly stable.

The Euro is a distant second at roughly 20%, followed by the Japanese Yen (~6%) and Pound Sterling (~5%). The Chinese Yuan — despite significant geopolitical push — holds merely ~2.3%, constrained by capital controls and limited financial market depth.

02 — The Petrodollar System

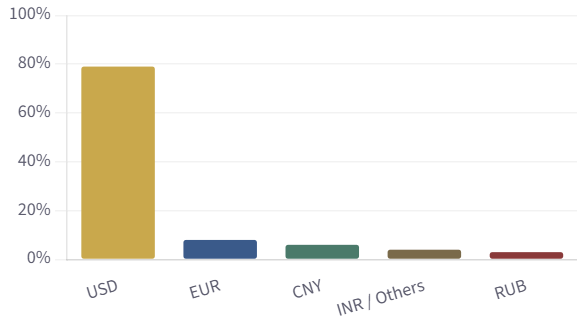

Oil Priced in Dollars: The Indispensable Anchor: The petrodollar system — born from the U.S.–Saudi agreement in 1974 — created a self-reinforcing loop: oil is priced and settled in USD globally, meaning every nation that imports oil must hold dollars. This single mechanism ensures perpetual global demand for the greenback, regardless of U.S. trade deficits

While there are growing experiments with yuan, rupee, and dirham-denominated oil trades (particularly between Russia, China, India, and Gulf states), these represent a small fraction of total flows. OPEC+ nations still invoice the overwhelming majority of crude exports in USD, keeping the structural architecture intact

“The petrodollar is not merely a trade mechanism — it is a geopolitical instrument. As long as oil remains the world’s primary energy input and is priced in dollars, the United States benefits from an extraordinary structural privilege: the ability to run persistent deficits financed by the rest of the world’s need to hold its currency” — Macro Strategy Desk Analysis

03 — Money Supply & Fed Policy

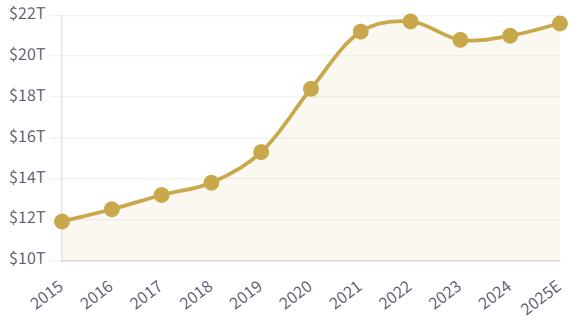

Dollar Printing: Exorbitant Privilege or Ticking Clock?: The U.S. Federal Reserve has the unique ability to create dollar liquidity that the entire world absorbs. During COVID-19 (2020–2021), the Fed expanded its balance sheet from ~$4T to over $9T — a near-doubling — yet the dollar remained the world’s safe-haven. This reflects the “exorbitant privilege” coined by French economist Valéry Giscard d’Estaing: the U.S. can finance its deficits in its own currency without the currency crisis that would befall any other nation.

The M2 money supply in the U.S. grew from approximately $15 trillion in 2019 to over $21 trillion by 2022. Despite this aggressive expansion, global dollar demand — driven by trade, debt servicing, and reserve accumulation — absorbed the excess supply, limiting the inflationary global spillover onto dollar dominance itself.

04 — Dollar Trade Dominance

SWIFT, Trade Finance & the Network Effect: Beyond oil and reserves, the dollar dominates because of deeply embedded network effects. Approximately 40% of global trade invoicing occurs in USD — far exceeding the U.S.’s share of world trade (~12%). SWIFT, the global financial messaging system, routes the majority of international transactions through dollar-clearing correspondent banks in New York.

This creates a sticky, self-reinforcing ecosystem: businesses invoice in dollars because counterparties expect it; banks hold dollar liquidity because loans are dollar-denominated; and sovereign borrowers issue dollar bonds because global investors demand them. The transition cost of shifting this network is enormous.

05 — The Road Ahead

USD Outlook: Structural Resilience, Gradual Erosion: The USD share in global reserves has declined from ~71% in 2000 to ~58% today — a shift, not a collapse. The rise of BRICS payment mechanisms, yuan internationalisation, and gold accumulation by emerging market central banks represent diversification, not displacement.

The key risks to monitor are: a significant loss of U.S. institutional credibility (fiscal dysfunction, debt ceiling crises), a viable deep-liquidity alternative emerging (unlikely before 2035), or a commodity market structural shift away from oil (long-term energy transition scenario).

The dollar’s throne is not under immediate threat. Its dominance rests on three interlocking pillars — financial network effects, the petrodollar system, and U.S. capital market depth — none of which can be dismantled overnight.