As we approach the final weeks of the financial year, we wanted to share an important market observation that has quietly played out for Indian equity investors over the past several years — something we call The April Theory.

What Is the April Theory?

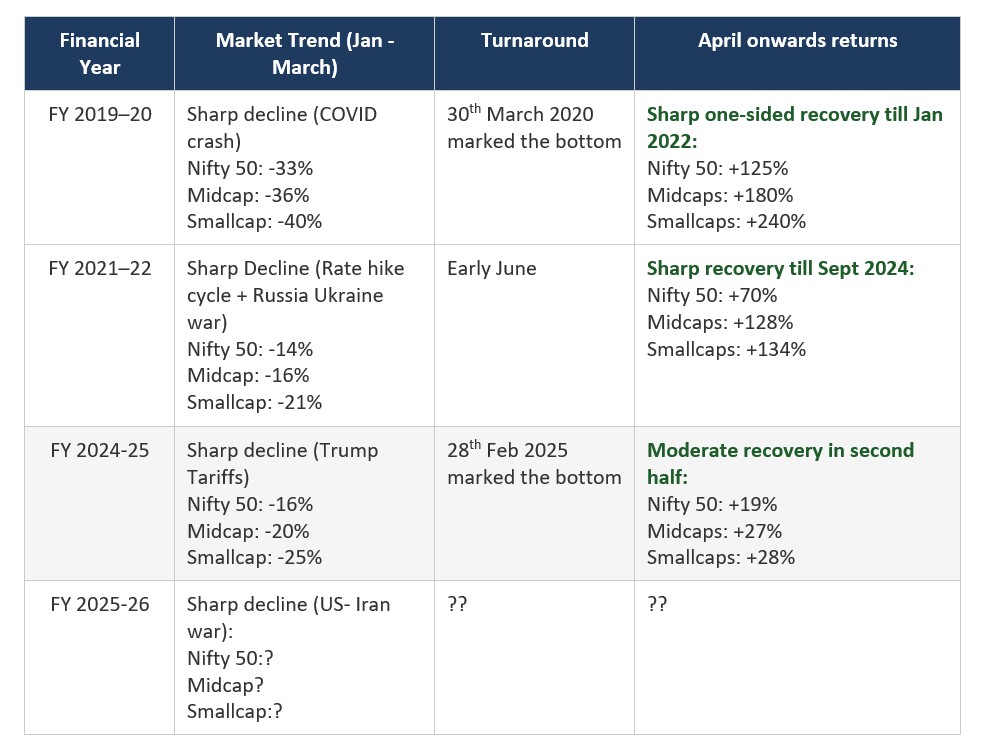

Every year, as India’s financial year draws to a close on March 31st, equity markets tend to witness a phase of selling pressure — often stretching from late February through mid-April. While this can feel unsettling in the moment, history suggests that this weakness is often temporary, and that April frequently marks the turning point for a fresh market upswing.

★ Key Insight: The April–June quarter has delivered positive returns in 8 out of the last 10 years for the Nifty 50 — making it one of the strongest seasonal windows in Indian equity markets.

The Data Speaks for Itself: Nifty 500 — Last 5 Years

Why Does This Happen? The Tax-Loss Harvesting Effect

The selling pressure into March is not random — it is driven by a well-known but often underappreciated behaviour: Tax-Loss Harvesting.

Indian investors must close their books by March 31st each year. Those who have made gains are liable to pay capital gains tax. To reduce this burden legally, many investors:

1. Identify loss-making holdings in their portfolio

2. Sell them before March 31st to “book” the losses officially

3. Offset these losses against their gains, reducing net taxable capital gains

4. Re-enter the market in April — redeploying capital at the start of the new financial year

Illustrative Example

An investor has ₹7 lakh in capital gains and also holds stocks with ₹3 lakh in unrealised losses.

By selling those loss-making stocks before March 31st, they reduce their taxable gains to just ₹4 lakh — saving significantly at both STCG (20%) and LTCG (12.5%) rates.

After April 1st, these investors return to the market — fuelling the seasonal recovery.

What Does This Mean for investors?

This seasonal pattern does not guarantee future performance, and markets can always surprise. However, the consistent presence of this dynamic suggests:

Market weakness in February–March should not be mistaken for a structural breakdown. Much of it is FY-end noise.

April often presents an attractive entry point — historically, investors who added to their portfolios during the March–April dip benefitted from the subsequent new-FY rebound.

Being patient through year-end volatility has historically been rewarded. Discipline at this juncture separates long-term wealth creators from reactive investors.