1. Stock prices are a slave of earnings: In the long run, valuation of a stock is nothing but the price that one pays for the future stream of the expected earnings and the dividends.

2. Volatility is your friend rather than your enemy. There’s a difference between risk and volatility: Risk is permanent loss of capital whereas volatility is unpredicted fluctuation in the stock market. Volatility is an inherent feature of the stock market and results in better returns for a disciplined investor.

Despite the short term volatilities, equity markets have created huge wealth for investors. Lumpsum investments in nifty has yielded an annual return of 12% whereas SIP has yielded around 14% since the year 2000.

3. The greatest long-term risk is not ‘loss of principal’ but ‘erosion of purchasing power’ as inflation tends to erode purchasing power of money over time.

4. A stock is an ownership stake in a business: A stock is seen by many as a cryptic piece of paper whose prices wiggles around continuously.

That’s one way to look at stocks. A far better way, suggested by Benjamin Graham, is to think of them as an ownership stake in an existing business. For eg- One of the reasons to invest in McDonalds stock is to have ownership in 40,000 real estate properties globally as McDonalds owns all the outlets run by its franchises on which it earns rent as well as royalty. The stock has appreciated from $2 in 1983 to $262 in 2023 – a yearly return of 18% excluding dividends.

5. Time in the market beats timing the market: Only two people know the top and bottom of the market: God & a liar. Therefore, it is a futile exercise to time the market (unless there is a black swan event taking the valuations to an extremely low level).

6. Odds of making money in the stock market increases as the time period increases.

7. Earlier the better – the power of compounding: Compounding even at modest rates, when done over a long period of time, produces truly spectacular outcomes

Achieving a CAGR of 100% for a few years is commendable, but achieving a CAGR of 20% for six decades is what makes a Warren Buffett. He played the game for the longest time and became the biggest winner.

8. Markets can remain irrational longer than you can remain solvent: It’s impossible to know when an overheated market will turn down, or when a downturn will cease and appreciation will take its place.

Isaac Newton was one of the early investors in South Sea Company. In 1720, the company bagged a deal to manage British government debt. As soon as the news spread, the price of the South Sea stock started soaring. Newton wisely chose to book profits in April and pocketed a handsome gain of about £20,000.As the euphoria around the stock kept on inching higher with every passing day, Newton could not resist the temptation of buying the hottest stock in town once again and invested nearly all his money in June that year and By October, the stock was worth less than a quarter of the price paid by Newton.

9. Great investing requires both generating returns and controlling risk. The risk reduces by 90% when the time period increases from 1 year to 10 years (in mutual funds):

10. Emotional Quotient is more important that Intelligent Quotients: It requires not only intelligence but also the emotional strength to be a good investor. Few know that Albert Einstein invested much of his 1921 Nobel Prize money in stock markets. However, he lost most of it in the 1929 stock market collapse.

Another classic example is the fall of Long-Term Capital Management – a hedge fund managing $126 billion in 1998. It was run by a team of Nobel Prize-winning economists and renowned Wall Street traders.

11. Don’t use leverage:

Whenever a really bright person who has a lot of money goes broke, it’s because of leverage. —Warren Buffett

Story of Rick Guerin – third partner at Berkshire:

“Charlie and I always knew that we would become incredibly wealthy. We were not in a hurry to get wealthy; we knew it would happen. Rick was just as smart as us, but he was in a hurry.” What happened was that in the 1973–1974 downturn, Rick was levered with margin loans. And the stock market went down almost 70% in those two years, so he got margin calls. He sold his Berkshire stock to Warren—Warren actually said “I bought Rick’s Berkshire stock”—at under $40 a piece”

Rick was forced to sell because he was levered. Today, one stock of Berkshire is around $ 4,72,000 (INR 4 cr.)

12. Another principle—simple, but easy to overlook—is that building wealth has little to do with your income or investment returns, and lots to do with your savings rate.

13. Don’t try to control what you can’t

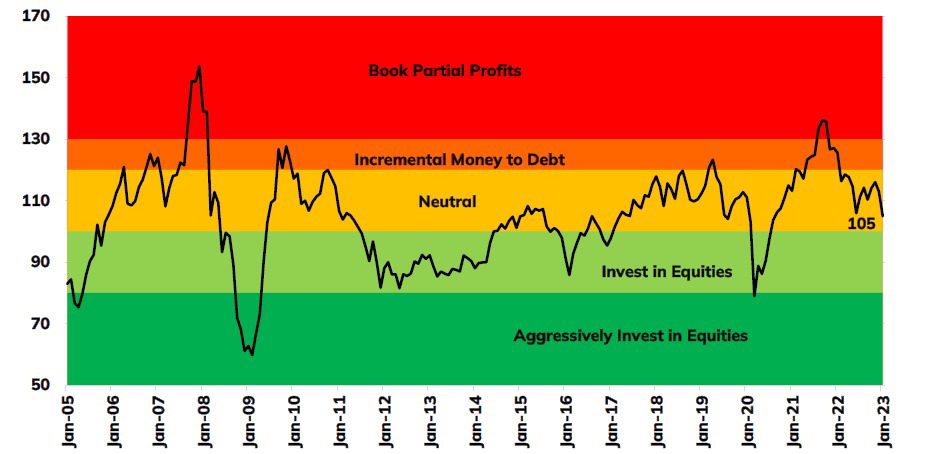

14. Market works in cycles

Economies and markets cycle up and down. Whichever direction they’re going at the moment, most people come to behave that they’ll go that way forever. To buy when others are despondently selling and to sell when others are euphorically buying takes the greatest courage, but provides the greatest profit. Always remember “The market’s not a very accommodating machine; it won’t provide high returns just because you need them.”

Over the period we have observed that investing is all about having the patience to hold on to your convictions. When you are unable to delay gratification, your greed is strong and it gets you in trouble in the financial markets.

15. Tune out the noise

We found a frontpage of a business daily, Mint published in May 2012 wherein all the negative headlines were published– High inflation, dollar depreciation & downgrade of Reliance stock (a situation similar to today) but here we are, in 2023, the Sensex has increased from 16,000 to 63,000 (4X jump), Reliance has increased from 345 to 2856 (8X jump) in the last 10 years.

Last but not the least, delegate the details: Financial professionals may help you create a customized portfolio strategy that’s built around your unique goals. Though no one can control markets, we can help you use them to pursue your long-term financial goals.